International trade payments: Exploring the available options

If you're expanding your business globally, then international trade payments can be overwhelming.

Whether you're buying or selling, the right international trade payment method is critical in reducing losses from bad debts, sustaining healthy profit margins and retaining healthy cash flow.

As technology expands to almost limitless trading ability across the world, so do the payment options. There are the tried and trusted traditional methods competing with digital transformation that challenge business ‘norms’ in the global cross border payment market. A market that is predicted to hit nearly $400 billion in the next 10 years.

To put that in perspective, the market's expected compound annual growth rate is over 7%.

Businesses that embrace the most efficient international trade payment methods will gain a significant advantage over their competitors. In this article, you'll find the top payment methods, pros and cons and the tools you need to start making efficient international trade payments.

The fundamentals of international trade payments

The last decade of globalization has accelerated the need for dynamic payment systems. It seems laughable that we can communicate and even travel around the world faster than we can make payments with some traditional methods.

When it comes to global cross border transactions, B2B payments dominate the industry. Nearly $40 trillion a year already flows across borders, a number which is expected to grow to $56 trillion by the end of the decade.

This is serious growth. It presents both an opportunity for businesses and an imperative need to optimize international payment strategies and workflows. If you don't, then your competitors will take advantage, unlocking global opportunities while you stay locked in the past.

Data on modern payment preferences is showing a shift in the way people are making their payments. For cross border purchases, 39% are made using credit cards, 26% using digital wallets, and 23% using debit cards.

But even these methods, particularly for larger international trade payments, aren't always the most suitable. Yes, they're quick and easy, but they can incur harsh costs.

Balancing risk and convenience

As with most things in the world, there's a trade off between risk, cost and convenience.

Traditional methods typically have higher costs and processing times. This is because they involve more regulation checks, with money passing through more intermediaries.

Compare that to some digital first solutions, where funds can move in a peer to peer fashion with reduced checks and balances. You gain speed and cost savings but sacrifice regulatory oversight.

The trick is to find the payment method that balances all of these factors for the optimal results.

Frameworks and methods of payment in international trade

So, where do you find this golden goose of payment methods? Next, we'll go into each type of payment method in international trade, including the pros and cons of each established framework.

Cash in advance

Cash in advance means the buyer pays for goods or services upfront before they're delivered. For a seller, it removes the risk of non payment before any cost is incurred. It's popular with exporters but creates troublesome cash flow for importers.

It's a common payment term for international trade, particularly if you are a new or perceived as a risky customer. In certain industries, to get your foot in the door, you might need to take this approach.

Of course, there's the added risk of a seller not meeting the agreed upon demands and holding on to the payment.

Documentary collections

Documentary collections offer a flexible but secure way to encourage international trade. It's more reliant on a level of trust between the buyer and the seller.

It works with an exporter sending shipping documents to their bank. The bank then forwards them to the importer's bank to make payment. The importer's bank then makes payment to the exporter's bank, and upon receipt of payment, the exporter's bank releases shipping documents for the importer.

It's a relatively simple, straightforward option and cost effective, with the exporter taking payment against shipping documents. Because the process works with payment being received before documents are released, it enhances security.

Adding to this, it's a universally accepted payment process built into globally recognized international trade payment frameworks.

While the process is straightforward, it can be slow, requiring the cooperation of multiple banks, and importers will need to pay in full before getting their hands on the goods.

Letters of credit

A letter of credit (LC) is a payment agreement that is underwritten with a guarantee from a bank. This ensures a seller receives payment from a buyer as long as certain conditions are met.

It offers more security and reduces risk for both exporters and importers. The buyer's bank issues a letter of credit to the exporter. The seller then ships goods, and the seller's bank uses the LC to request payment from the buyer's bank.

It's a valuable way to build trust between two parties. Plus, an LC can actually be used for finance arrangements to ease cash flow for buyers. Also, if a buyer defaults on a payment, a seller's bank can still receive payment from the buyer's bank, as the payment is guaranteed.

It's a highly trustworthy method but runs up high costs with fees from issuing banks that include charges for the issuance, management, negotiation and any amendments to the LC.

Open account trading

Open account trading provides credit from the seller to the buyer. This generally offers a payment after delivery, which could be anywhere between 30 and 90 days.

For buyers, it has favorable terms to gain an advantage. You can purchase products or services and sell them before ever even paying the seller.

It requires a high level of trust between both parties as the seller is relinquishing their products long before they receive payment.

While this might sound like unfavorable terms, as a seller or exporter, it can offer competitive advantages in attracting companies with cash flow restraints.

Open accounting creates more administration and more complicated payment workflows for companies, which is why a growing number of companies are moving to real time payment solutions. In fact, reports show that 92% of businesses are planning to invest in real time payment solutions for their open account transactions.

Consignment arrangements

Consignment arrangements enable a business to sell goods on behalf of the manufacturing or supplying company, the ‘consignor’.

The clever part about this arrangement is the selling business, the ‘consignee’, never actually purchases the stock. Sell it and take a commission for the sale.

This is a common practice in high value B2C industries. For example, a bike shop stocks high end products without purchasing them from the supplier. Once a bike is sold, the bike shop takes a commission and pays the rest to the actual owner.

Obviously, there are clear benefits to the consignee who never actually has to purchase stock upfront, reducing the financial risk and burden. Plus, it allows them to tap into a broader market and assortment of products for their customers.

What payment options are available for international transactions?

Once you've established payment frameworks for your international payments, you need to understand how you're actually going to move money. Here’s a breakdown of the best payment platforms:

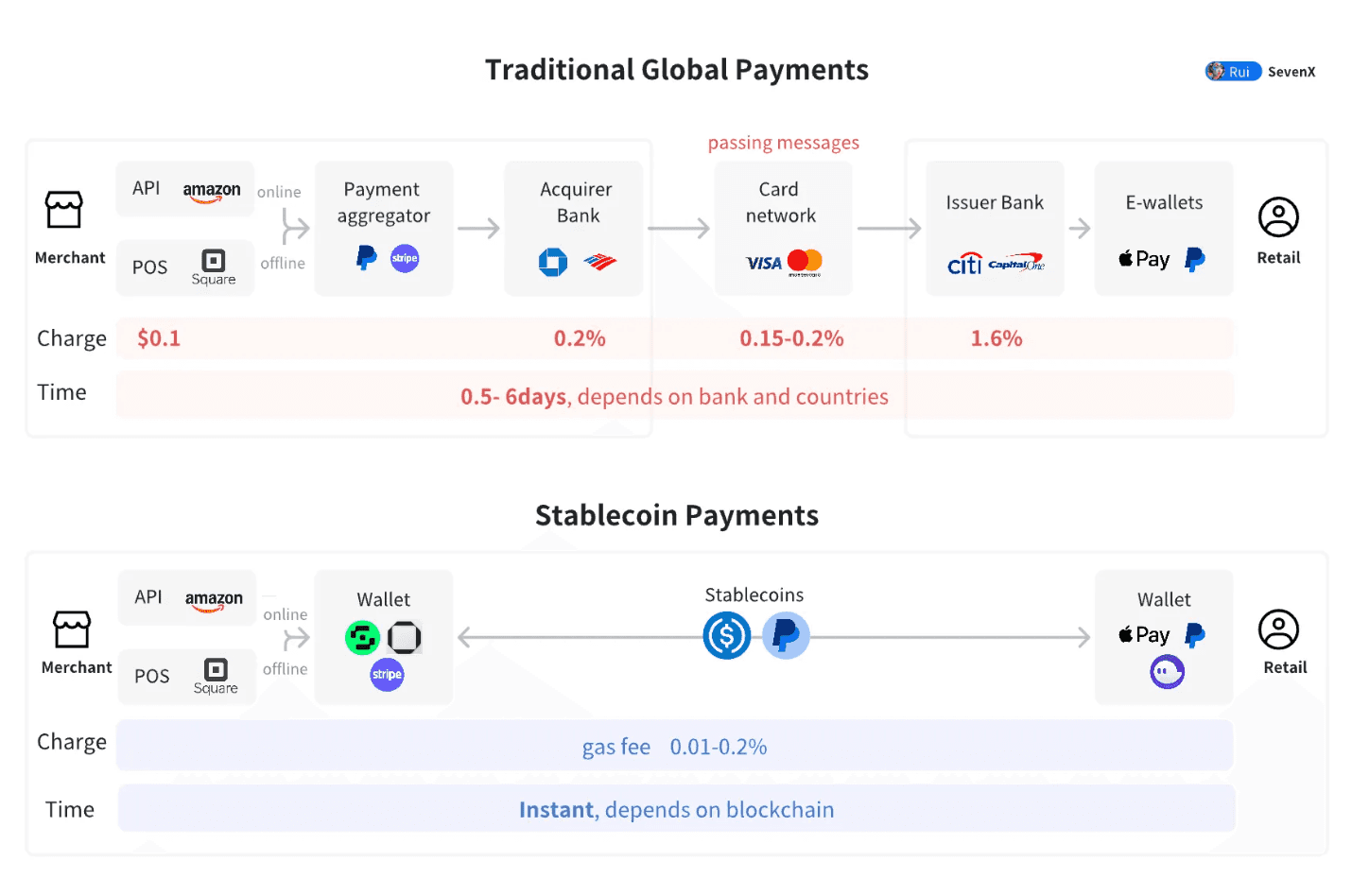

1. Traditional banking rails

When working with any of the above established payment workflows, such as cash in advance or open accounting, traditional banking is a secure payment method for trade transactions.

Wire transfers allow buyers to make a direct transfer from one bank account to another. Credit cards are also widely accepted but tend to be reserved for smaller transactions.

The big problem with traditional banking methods is speed and cost. Both wire transfers and credit cards can rack up huge fees, up to 5% and more in the worst case scenarios.

Plus, if you're moving across currencies, then you might find yourself with unfavorable exchange rates, adding to the cost further. All of this is burdened with slow processing times. It's not uncommon for payments to take three to five days to complete.

2. Digital payment platforms

High costs and slow speeds are why digital payment platforms are capturing more of the market. For businesses regularly making cross border payments in multiple currencies, they offer a gateway to do business in hundreds of currencies across hundreds of countries. It makes it easy for a business to pivot in and out of markets while accepting and sending local payment methods.

Platforms like PayPal are well known, but while they have fast payments, they can still be expensive when it comes to fees. Wise (formerly TransferWise) is another popular alternative. While it’s quick and cheap, it creates a headache of having to manage multi currency accounts and has limited geographical reach in certain jurisdictions.

Compare that to Acctual, which allows complete flexibility in your international trade payments. There are no better solutions on the market. Acctual enables you to both send and receive funds in your chosen currency while automatically doing the same for your trade partner.

Plus, you can even integrate stablecoin cryptocurrencies into your payment workflow.

It's a platform born out of the direct frustration of business owners who say they are unnecessarily paying high fees for their cross border payments.

3. Blockchain and cryptocurrency payments

The most significant use case for cryptocurrency is global cross border transactions. Its peer to peer design enables one person or entity to send funds directly to another person or entity. Crypto leaves the sender's wallet and arrives directly in the recipient's crypto wallet in a matter of seconds for just a few cents. There's no need for intermediary banks or third party trust.

If you're worried about volatility, then stablecoins like USDC or USDT are pegged to the US dollar. That means one coin is always worth one dollar. From a value point of view, they act like a digital dollar, but from a technological standpoint, they operate like a cryptocurrency.

When integrated into digital payment platforms, it gives you unparalleled global reach to make and receive payments almost anywhere in the world.

With speeds bordering on instantaneous and cost savings of 90+ per cent, businesses that start developing payment workflows that integrate cryptocurrency will enjoy a competitive advantage.

4. Supply chain finance

When it comes to managing cash flow for your global trade payments, using financial instruments like reverse factoring can help you get paid earlier through your invoicing and contracting.

It allows a seller to enjoy financing from a bank to improve cash flow before the buyer needs to settle the bill.

If you've only ever dealt in cash payments, then invoice factoring can be intimidating at first, but it can have strategic advantages that help improve supplier relationships long term.

5. Escrow services

An escrow service uses a third party to hold funds until a contractual obligation is fulfilled. It offers a neutral party to create peace of mind for both parties in a deal. It helps to add trust where it otherwise might not exist. This can be particularly helpful in new global trade arrangements where partners are still establishing a relationship.

Some digital platforms can integrate escrow processes into your international trade, and automation has even helped to reduce the cost and complexity of these escrow services, so it's become more viable even for smaller transactions than in the past.

But you still might expect added costs that could reach 5% plus other transaction fees. So it can get expensive, but it might be necessary when making large one off payments with unfamiliar partners.

Strategic management of international trade payments

Throughout your international trade payments, you'll need to strategically manage your payment workflows. This includes risks, compliance and efficiency.

1. Risk assessment and mitigation

When assessing credit risk, you should do your research on both the company partner and any country specific angles. For example, even if your partner is a financially sound company, there could be issues at a more regional or country level.

Unstable governments issuing currency controls, OFAC list restrictions, or risks of hyperinflation could expose you to unnecessarily high risk. If it's a deal breaker, you could look at political risk insurance for volatile reasons, which could add 1 to 3% to a transaction value.

2. Foreign exchange risk management

If you're managing multi currency accounts, then currency fluctuation can quickly erode profit margins. You could easily see 2 to 5% disappear without careful management. In B2B industries where margins are thin, that can quickly turn a profitable deal into a loss if the exchange rate moves against you.

Forward contracts can help you lock in exchange rates in the future to give you complete certainty in your business dealings, or establishing payment currencies with your partners from day one can negate the need for multi currency accounts and avoid losing money on currency fees and market spreads.

3. Compliance and regulatory considerations

When you're making global cross border payments, anti money laundering requirements are becoming ever more stringent. Your policies and processes need to be regularly updated to make sure you adhere to guidelines.

Adding to this, Know Your Customer (KYC) is extending across multiple levels of business relationships, not just a requirement for banks anymore. As a company, you need to have full visibility of both your trading partners and their compliance throughout the supply chain.

Any failures could lead to heavy penalties, which can put severe pressure on even the most robust businesses.

Adding to this, there are tax implications too, which can vary based on payment method, timing and jurisdictions. Particularly if you're starting to incorporate cryptocurrency into your payment flow, many jurisdictions treat crypto as property rather than currency.

Integrating technology into your payment workflow can add automation that reduces processing costs by up to 80% while also improving accuracy. A result that improves profitability and ensures stable relationships with trading partners. Plus, it can take reconciliation times for all payments to minutes rather than days.

Flexible international trade payments with Acctual

Acctual small business invoicing offers unrivalled flexibility for making international trade payments.

It eliminates the need for multiple systems in your payment workflow. That means no more multi currency accounts, excessive fees, or manual data entry.

As a supplier, you can easily send invoices that allow your client to pay how they like while you receive funds in your preferred currency. That includes fiat to crypto payments, vice versa and everything in between. All for transaction fees significantly lower than traditional payment methods.

For example, a Colombian importer can pay in USDT or USDC while a vendor in the US receives the payment in USD the same day.

Acctual takes care of everything automatically, all with built in KYC verification.

Plus, everything smoothly integrates with your accounting and ERP system to remove the headache of multi currency payments or moving money between business entities.

So if you're trying to work out what payment options are available for international transactions, take two minutes to get started with Acctual for your international trade payments today.

International trade payments: Exploring the available options

If you're expanding your business globally, then international trade payments can be overwhelming.

Whether you're buying or selling, the right international trade payment method is critical in reducing losses from bad debts, sustaining healthy profit margins and retaining healthy cash flow.

As technology expands to almost limitless trading ability across the world, so do the payment options. There are the tried and trusted traditional methods competing with digital transformation that challenge business ‘norms’ in the global cross border payment market. A market that is predicted to hit nearly $400 billion in the next 10 years.

To put that in perspective, the market's expected compound annual growth rate is over 7%.

Businesses that embrace the most efficient international trade payment methods will gain a significant advantage over their competitors. In this article, you'll find the top payment methods, pros and cons and the tools you need to start making efficient international trade payments.

The fundamentals of international trade payments

The last decade of globalization has accelerated the need for dynamic payment systems. It seems laughable that we can communicate and even travel around the world faster than we can make payments with some traditional methods.

When it comes to global cross border transactions, B2B payments dominate the industry. Nearly $40 trillion a year already flows across borders, a number which is expected to grow to $56 trillion by the end of the decade.

This is serious growth. It presents both an opportunity for businesses and an imperative need to optimize international payment strategies and workflows. If you don't, then your competitors will take advantage, unlocking global opportunities while you stay locked in the past.

Data on modern payment preferences is showing a shift in the way people are making their payments. For cross border purchases, 39% are made using credit cards, 26% using digital wallets, and 23% using debit cards.

But even these methods, particularly for larger international trade payments, aren't always the most suitable. Yes, they're quick and easy, but they can incur harsh costs.

Balancing risk and convenience

As with most things in the world, there's a trade off between risk, cost and convenience.

Traditional methods typically have higher costs and processing times. This is because they involve more regulation checks, with money passing through more intermediaries.

Compare that to some digital first solutions, where funds can move in a peer to peer fashion with reduced checks and balances. You gain speed and cost savings but sacrifice regulatory oversight.

The trick is to find the payment method that balances all of these factors for the optimal results.

Frameworks and methods of payment in international trade

So, where do you find this golden goose of payment methods? Next, we'll go into each type of payment method in international trade, including the pros and cons of each established framework.

Cash in advance

Cash in advance means the buyer pays for goods or services upfront before they're delivered. For a seller, it removes the risk of non payment before any cost is incurred. It's popular with exporters but creates troublesome cash flow for importers.

It's a common payment term for international trade, particularly if you are a new or perceived as a risky customer. In certain industries, to get your foot in the door, you might need to take this approach.

Of course, there's the added risk of a seller not meeting the agreed upon demands and holding on to the payment.

Documentary collections

Documentary collections offer a flexible but secure way to encourage international trade. It's more reliant on a level of trust between the buyer and the seller.

It works with an exporter sending shipping documents to their bank. The bank then forwards them to the importer's bank to make payment. The importer's bank then makes payment to the exporter's bank, and upon receipt of payment, the exporter's bank releases shipping documents for the importer.

It's a relatively simple, straightforward option and cost effective, with the exporter taking payment against shipping documents. Because the process works with payment being received before documents are released, it enhances security.

Adding to this, it's a universally accepted payment process built into globally recognized international trade payment frameworks.

While the process is straightforward, it can be slow, requiring the cooperation of multiple banks, and importers will need to pay in full before getting their hands on the goods.

Letters of credit

A letter of credit (LC) is a payment agreement that is underwritten with a guarantee from a bank. This ensures a seller receives payment from a buyer as long as certain conditions are met.

It offers more security and reduces risk for both exporters and importers. The buyer's bank issues a letter of credit to the exporter. The seller then ships goods, and the seller's bank uses the LC to request payment from the buyer's bank.

It's a valuable way to build trust between two parties. Plus, an LC can actually be used for finance arrangements to ease cash flow for buyers. Also, if a buyer defaults on a payment, a seller's bank can still receive payment from the buyer's bank, as the payment is guaranteed.

It's a highly trustworthy method but runs up high costs with fees from issuing banks that include charges for the issuance, management, negotiation and any amendments to the LC.

Open account trading

Open account trading provides credit from the seller to the buyer. This generally offers a payment after delivery, which could be anywhere between 30 and 90 days.

For buyers, it has favorable terms to gain an advantage. You can purchase products or services and sell them before ever even paying the seller.

It requires a high level of trust between both parties as the seller is relinquishing their products long before they receive payment.

While this might sound like unfavorable terms, as a seller or exporter, it can offer competitive advantages in attracting companies with cash flow restraints.

Open accounting creates more administration and more complicated payment workflows for companies, which is why a growing number of companies are moving to real time payment solutions. In fact, reports show that 92% of businesses are planning to invest in real time payment solutions for their open account transactions.

Consignment arrangements

Consignment arrangements enable a business to sell goods on behalf of the manufacturing or supplying company, the ‘consignor’.

The clever part about this arrangement is the selling business, the ‘consignee’, never actually purchases the stock. Sell it and take a commission for the sale.

This is a common practice in high value B2C industries. For example, a bike shop stocks high end products without purchasing them from the supplier. Once a bike is sold, the bike shop takes a commission and pays the rest to the actual owner.

Obviously, there are clear benefits to the consignee who never actually has to purchase stock upfront, reducing the financial risk and burden. Plus, it allows them to tap into a broader market and assortment of products for their customers.

What payment options are available for international transactions?

Once you've established payment frameworks for your international payments, you need to understand how you're actually going to move money. Here’s a breakdown of the best payment platforms:

1. Traditional banking rails

When working with any of the above established payment workflows, such as cash in advance or open accounting, traditional banking is a secure payment method for trade transactions.

Wire transfers allow buyers to make a direct transfer from one bank account to another. Credit cards are also widely accepted but tend to be reserved for smaller transactions.

The big problem with traditional banking methods is speed and cost. Both wire transfers and credit cards can rack up huge fees, up to 5% and more in the worst case scenarios.

Plus, if you're moving across currencies, then you might find yourself with unfavorable exchange rates, adding to the cost further. All of this is burdened with slow processing times. It's not uncommon for payments to take three to five days to complete.

2. Digital payment platforms

High costs and slow speeds are why digital payment platforms are capturing more of the market. For businesses regularly making cross border payments in multiple currencies, they offer a gateway to do business in hundreds of currencies across hundreds of countries. It makes it easy for a business to pivot in and out of markets while accepting and sending local payment methods.

Platforms like PayPal are well known, but while they have fast payments, they can still be expensive when it comes to fees. Wise (formerly TransferWise) is another popular alternative. While it’s quick and cheap, it creates a headache of having to manage multi currency accounts and has limited geographical reach in certain jurisdictions.

Compare that to Acctual, which allows complete flexibility in your international trade payments. There are no better solutions on the market. Acctual enables you to both send and receive funds in your chosen currency while automatically doing the same for your trade partner.

Plus, you can even integrate stablecoin cryptocurrencies into your payment workflow.

It's a platform born out of the direct frustration of business owners who say they are unnecessarily paying high fees for their cross border payments.

3. Blockchain and cryptocurrency payments

The most significant use case for cryptocurrency is global cross border transactions. Its peer to peer design enables one person or entity to send funds directly to another person or entity. Crypto leaves the sender's wallet and arrives directly in the recipient's crypto wallet in a matter of seconds for just a few cents. There's no need for intermediary banks or third party trust.

If you're worried about volatility, then stablecoins like USDC or USDT are pegged to the US dollar. That means one coin is always worth one dollar. From a value point of view, they act like a digital dollar, but from a technological standpoint, they operate like a cryptocurrency.

When integrated into digital payment platforms, it gives you unparalleled global reach to make and receive payments almost anywhere in the world.

With speeds bordering on instantaneous and cost savings of 90+ per cent, businesses that start developing payment workflows that integrate cryptocurrency will enjoy a competitive advantage.

4. Supply chain finance

When it comes to managing cash flow for your global trade payments, using financial instruments like reverse factoring can help you get paid earlier through your invoicing and contracting.

It allows a seller to enjoy financing from a bank to improve cash flow before the buyer needs to settle the bill.

If you've only ever dealt in cash payments, then invoice factoring can be intimidating at first, but it can have strategic advantages that help improve supplier relationships long term.

5. Escrow services

An escrow service uses a third party to hold funds until a contractual obligation is fulfilled. It offers a neutral party to create peace of mind for both parties in a deal. It helps to add trust where it otherwise might not exist. This can be particularly helpful in new global trade arrangements where partners are still establishing a relationship.

Some digital platforms can integrate escrow processes into your international trade, and automation has even helped to reduce the cost and complexity of these escrow services, so it's become more viable even for smaller transactions than in the past.

But you still might expect added costs that could reach 5% plus other transaction fees. So it can get expensive, but it might be necessary when making large one off payments with unfamiliar partners.

Strategic management of international trade payments

Throughout your international trade payments, you'll need to strategically manage your payment workflows. This includes risks, compliance and efficiency.

1. Risk assessment and mitigation

When assessing credit risk, you should do your research on both the company partner and any country specific angles. For example, even if your partner is a financially sound company, there could be issues at a more regional or country level.

Unstable governments issuing currency controls, OFAC list restrictions, or risks of hyperinflation could expose you to unnecessarily high risk. If it's a deal breaker, you could look at political risk insurance for volatile reasons, which could add 1 to 3% to a transaction value.

2. Foreign exchange risk management

If you're managing multi currency accounts, then currency fluctuation can quickly erode profit margins. You could easily see 2 to 5% disappear without careful management. In B2B industries where margins are thin, that can quickly turn a profitable deal into a loss if the exchange rate moves against you.

Forward contracts can help you lock in exchange rates in the future to give you complete certainty in your business dealings, or establishing payment currencies with your partners from day one can negate the need for multi currency accounts and avoid losing money on currency fees and market spreads.

3. Compliance and regulatory considerations

When you're making global cross border payments, anti money laundering requirements are becoming ever more stringent. Your policies and processes need to be regularly updated to make sure you adhere to guidelines.

Adding to this, Know Your Customer (KYC) is extending across multiple levels of business relationships, not just a requirement for banks anymore. As a company, you need to have full visibility of both your trading partners and their compliance throughout the supply chain.

Any failures could lead to heavy penalties, which can put severe pressure on even the most robust businesses.

Adding to this, there are tax implications too, which can vary based on payment method, timing and jurisdictions. Particularly if you're starting to incorporate cryptocurrency into your payment flow, many jurisdictions treat crypto as property rather than currency.

Integrating technology into your payment workflow can add automation that reduces processing costs by up to 80% while also improving accuracy. A result that improves profitability and ensures stable relationships with trading partners. Plus, it can take reconciliation times for all payments to minutes rather than days.

Flexible international trade payments with Acctual

Acctual small business invoicing offers unrivalled flexibility for making international trade payments.

It eliminates the need for multiple systems in your payment workflow. That means no more multi currency accounts, excessive fees, or manual data entry.

As a supplier, you can easily send invoices that allow your client to pay how they like while you receive funds in your preferred currency. That includes fiat to crypto payments, vice versa and everything in between. All for transaction fees significantly lower than traditional payment methods.

For example, a Colombian importer can pay in USDT or USDC while a vendor in the US receives the payment in USD the same day.

Acctual takes care of everything automatically, all with built in KYC verification.

Plus, everything smoothly integrates with your accounting and ERP system to remove the headache of multi currency payments or moving money between business entities.

So if you're trying to work out what payment options are available for international transactions, take two minutes to get started with Acctual for your international trade payments today.

Blog

Create the world’s most flexible invoice in seconds

With

from NYC

Guides

Invoice NO

0001

From

Marble Studio

billing@marble.studio

To

Charm AI

billing@charm.ai

Amount

$20,800.00

Due by

May 19, 2026

PAYMENT METHOD

Bank

Card

Crypto

Invoice NO

0001

From

Adria Studio

payments@adria.studio

To

Charm AI

billing@charm.ai

Amount

$20,800.00

Due by

May 19, 2026

Method

USDC via ETH/Solana

Invoice NO

0001

From

Marble Studio

billing@marble.studio

To

Acctual

payables@acctual.com

Amount

$20,800.00

Due by

May 19, 2026

PAYMENT METHOD

USDC via ETH/Solana

Create the world’s most flexible invoice in seconds

With

from NYC

Guides

Invoice NO

0001

From

Marble Studio

billing@marble.studio

To

Charm AI

billing@charm.ai

Amount

$20,800.00

Due by

May 19, 2026

PAYMENT METHOD

Bank

Card

Crypto

Invoice NO

0001

From

Adria Studio

payments@adria.studio

To

Charm AI

billing@charm.ai

Amount

$20,800.00

Due by

May 19, 2026

Method

USDC via ETH/Solana

Invoice NO

0001

From

Marble Studio

billing@marble.studio

To

Acctual

payables@acctual.com

Amount

$20,800.00

Due by

May 19, 2026

PAYMENT METHOD

USDC via ETH/Solana

Create the world’s most flexible invoice in seconds

With

from NYC

Guides